THE INTERGENERATIONAL TRANSMISSION OF WEALTH

Motivating questions

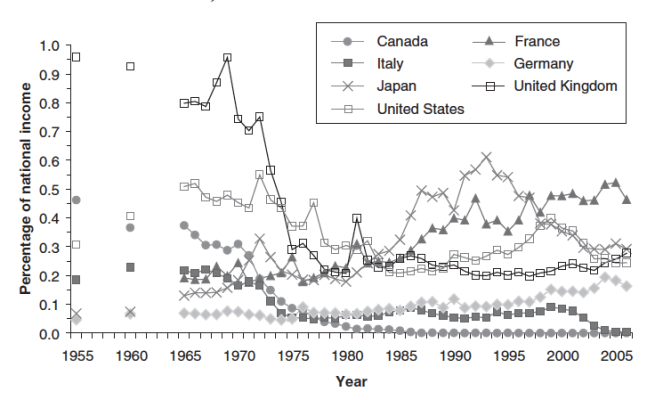

How concentrated is the distribution of wealth, and what fraction of individual wealth holdings is due to inheritances? These basic facts can help motivate our understanding of the implications of the rising share of income among the top 1 % for intergenerational dynamics.

This lecture also introduces us to the empirical analysis of intergenerational transmission of economic status. Top end inequality has its most obvious intergenerational implication in terms of the transmission of financial resources, namely assets, and so we also want to develop an understanding of the strength of the relationship between parent and child wealth: how is this measured? what are the data challenges? and finally what are the best estimates of the intergenerational wealth correlations?

Finally, the policy implications this lecture focuses upon is inheritance taxation. Robin Boadway and his co-authors discuss different theoretical rationale for introducing such taxes, from “welfarism” to “equality of opportunity.” It is important to be aware of these theoretical perspectives so that we can also appreciate the many important design features and trade-offs in assessing policy proposals.

You can also download supplementary Lecture 4 Slides that cover the other readings.

Explore these according to your interest and to be able to follow the conversation, but that said be certain to include the Kuhn, Schularick and Steins paper among your readings.

Main readings

OECD (2011). Divided We Stand: Why Inequality Keeps Rising. OECD Publishing. https://www.oecd-ilibrary.org/social-issues-migration-health/the-causes-of-growing-inequalities-in-oecd-countries_9789264119536-en

Kuhn, Moritz, Moritz Schularick, and Ulrike I. Steins (2018). “Income and Wealth Inequality in America, 1949-2016.” Opportunity and Inclusive Growth Institute, Federal Reserve Bank of Minneapolis, Institute Working Paper 9.

Alvaredo, Facundo, Bertrand Garbinti, and Thomas Piketty (2017). “On the Share of Inheritance in Aggregate Wealth: Europe and the USA, 1900-2010.” Economica. 84, 239-260.

Clark, Gregory and Neil Cummins (2014). “Intergenerational Wealth Mobility in England, 1858-2012.” Economic Journal. 125 (February): 61-85.

Pfeffer, Fabian T. and Alexandra Killewald (2018). “Generations of Advantage. Multigenerational Correlations in Family Wealth.” Social Forces. 96 (4): 1411-1442.

Boserup, Simon Halphen, Wojciech Kopczuk, and Claus Trustrup Kreiner (2017). “Intergenerational Wealth Formation over the Life Cycle: Evidence from Danish Wealth Records 1984-2013.” Unpublished manuscript.

Adermon, Adrian, Mikael Lindahl, and Daniel Waldenström (2018). “Intergenerational Wealth Mobility and the Role of Inheritance: Evidence from Multiple Generations.” Economic Journal. 128 (612): 482–513.

Boadway, Robin, Emma Chamberlain, and Carl Emmerson (2008). “Taxation of Wealth and Wealth Transfers.” In Institute for Fiscal Studies (editor). Mirrlees Review: Dimensions of Tax Design. Chapter 8. Oxford: Oxford University Press.

Batchelder, Lily (2018). “How to Make Trump-Style Wealth Pay Its Fair Share.” New York Times. Opinion Section, October 4.

Mankiw, Gregory N. (2000). “The Estate Tax is one Death Penalty too Many.” Fortune. September 4.