The COVID19 crisis has unleashed an economic crisis that is unprecedented in its speed and in its depth, making these very interesting times to study macro-economics.

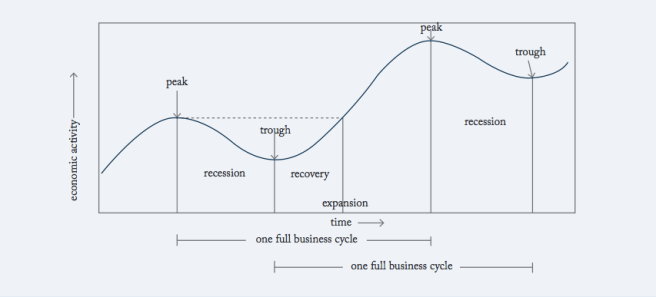

Lecture 9 of Economics for Everyone describes the anatomy of the business cycle, and relates these swings in macroeconomic activity to a statistic that, as much as any other, speaks directly to the lives of citizens, the unemployment rate.

So in this lecture we describe the anatomy of the business cycle, how macro-economists link changes in GDP from its potential to changes in the unemployment rate, and finally just exactly what is this statistic called the “unemployment rate” and how is it measured by statistical agencies.

In this eighth lecture of Economics for Everyone, we begin our discussion of macroeconomics, the study of the overall level of economic activity.

The lecture offers some background and motivation by examining the sharp increase and sluggish fall of the unemployment rate during the 1930s, the Great Depression. This led to a crisis in economic thinking, and to the publication of John Maynard Keynes’s “General Theory”. Thus macro-economics was born.

Our first challenge involves a host of measurement issues, and in this lecture we examine the meaning, the measurement and the use of Gross Domestic Product. This statistic is nicely presented, reviewed, and evaluated in Diane Coyle’s book, GDP: A Brief but Affectionate History, and it is the major reading on your list for this lecture.

In this seventh lecture of Economics for Everyone, we address the nature of government intervention in perfectly competitive markets.

Perfectly competitive markets lead to efficient outcomes, in the sense that no one can be made better off without making someone worse off. But that doesn’t mean we like the outcomes, that they are fair or justice, and as a result governments are often pressured, or even captured, to intervene, sometimes not for the broader social good, but for the benefit of a few to the cost of many.

At the same time competitive markets don’t always lead to efficient outcomes because prices don’t may not reflect all social costs and benefits. So we may have too much, or too little ,of some goods if we let the market work. Governments are often pressure to intervene for the benefit of many, but also at the costs of some.

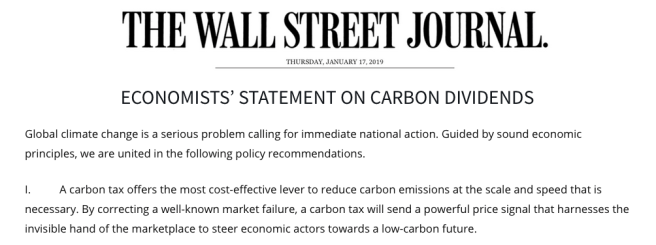

In this lecture, we work through a number of practical examples to illustrate rent-seeking behaviour in which a group can capture government policy to their benefit, and we also discuss market failures, and the consensus view of economists that these should be corrected with appropriate taxation. Agricultural support programs are one example, and putting a price on carbon is another.

“We might as reasonably dispute,” Alfred Marshall wrote in his famous economics textbook first published in 1890, “whether it is the upper or the under blade of a pair of scissors that cuts a piece of paper, as whether value is governed by utility or cost of production.”

Prices are determined in the marketplace, through the communication between buyers and sellers, jointly through a negotiation reflecting their willingness to pay, and their costs of offering. Marshall offered us these tools, the demand curve and the supply curve, to understand price determination in perfectly competitive markets. And he also characterized them, and used them to illustrate price determination in a wide variety of examples.

As a part of this he introduced the notion of “elasticity,” a concept that Congresswoman Alexandria Ocasio-Cortez learned well in her economics courses, and used to drive home what she felt were some important lessons in understanding health care. Listen to her.

And so this week’s class in our course, Economics for Everyone, is about elasticity. If she can understand it, so can you. If she can use it, so can you. And that is what we do in the lecture: define the concept, and show how it is used to understand market outcomes for some policy relevant examples.

In a free market, people don’t buy things that are worth less to them than the asking price. And people don’t sell things that are worth more to them the asking price. … The reason is simple: nobody is forcing them to, which means that most transactions that happen in a free market improve efficiency, because they make both parties better off—or at least not worse off–and don’t harm anyone else.

The chapter of his book called “Perfect Markets and the ‘World of Truth'” is the starting point and the end point of the next block of lectures in our course Economics for Everyone. Harford is describing both the power of markets, and the potential for their failures, big and small. He is describing what economics call the two fundamental theorems of welfare economics, and in order to do so he has to explore the determination of relative prices, the neoclassical theory of value.

In perfectly competitive markets we can describe the determination of prices in terms of demand and supply curves. And so we have to develop a facility in using these tools to understand how markets work, how they are sometimes manipulated for better or for worse, and how they may fail in a way that can rationalize a role for public policy.

One survey of professional economists in the United States found that 93% would agree with the claim that restrictions on free trade through tariffs and import quotas would reduce economic welfare.

Yet, I’m certain those advocating for free trade are often accused of having a blind spot. Is there something in the economic method, which can legitimately lay claim to being scientific, that also blinds its practitioners to what others see so clearly?

“We might as reasonably dispute,” Alfred Marshall wrote in his famous economics textbook first published in 1890, “whether it is the upper or the under blade of a pair of scissors that cuts a piece of paper, as whether value is governed by utility or cost of production.”

“We might as reasonably dispute,” Alfred Marshall wrote in his famous economics textbook first published in 1890, “whether it is the upper or the under blade of a pair of scissors that cuts a piece of paper, as whether value is governed by utility or cost of production.”