In this seventh lecture of Economics for Everyone, we address the nature of government intervention in perfectly competitive markets.

Perfectly competitive markets lead to efficient outcomes, in the sense that no one can be made better off without making someone worse off. But that doesn’t mean we like the outcomes, that they are fair or justice, and as a result governments are often pressured, or even captured, to intervene, sometimes not for the broader social good, but for the benefit of a few to the cost of many.

At the same time competitive markets don’t always lead to efficient outcomes because prices don’t may not reflect all social costs and benefits. So we may have too much, or too little ,of some goods if we let the market work. Governments are often pressure to intervene for the benefit of many, but also at the costs of some.

In this lecture, we work through a number of practical examples to illustrate rent-seeking behaviour in which a group can capture government policy to their benefit, and we also discuss market failures, and the consensus view of economists that these should be corrected with appropriate taxation. Agricultural support programs are one example, and putting a price on carbon is another.

Download the presentation for Lecture 7, “Understanding public policy in competitive markets” as a pdf, and if you like listen to narrated version.

I found the illustrations of the quotas, price supports and deficiency payments very helpful. As I answered the questions in the initial assignment, I considered them just from a logical point of view, not fully realizing that the impact of each program on each group could be calculated mathematically. I think others have brought this up at some point, but I wonder, is it possible to illustrate one of these programs with actual supply and demand curves based on data, ie, can we see a real-life example of these illustrations? Of course, as a non-math person, I don’t want to be dragged toooo far into the weeds on this.

Thank you for illustrating the so-called price gouging regarding supplies during this COVID outbreak (and as I’m typing this, I received this from Notify NYC: Notify NYC: If you see price increases for items in short supply due to COVID-19, report it by calling 311 or visiting NYC.gov/dcwp). As you know, I thought of this the other day when I saw a in a tweet that oranges and orange juice were going to be in high demand in the coming season. I envisioned a supply/demand chart with inelastic supply (because you can’t just make more oranges grow within the season) and a demand curve shifted to the right, which in turn, makes the price equilibrium higher. That is pretty much what you illustrated in the lecture, so I feel I am grasping this.

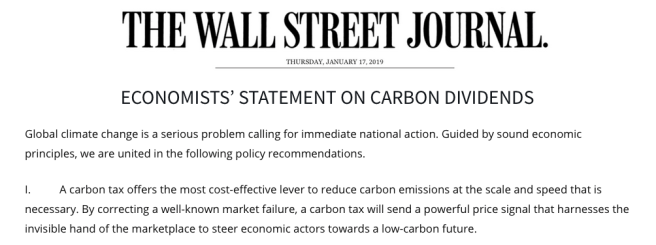

Finally, the carbon tax document was interesting — but frustrating to see so many intelligent people agree on a policy that we cannot summon the political will to enact.

Oh and thanks for (not really) sharing the chocolate!

Thanks so much for this Vince, you are indeed becoming an “Undercover Economist”.

I’m not certain that I will be able to find specific estimates of the demand elasticities for these commodities, but I agree that would offer a valuable teaching tool. I’ll give it a try, or at least point people to some official websites that describe the programs. But keep in mind, one of the purposes of this is not simply to understand the markets for particular agricultural commodities, but also to exercise our use of these tools so that we can bring them to other issues we may encounter.

That said, I think the externalities issue would be particularly relevant to you, given your interest in urban planning. I believe that Harford illustrates this with respect to traffic congestion, and the proposed congestion tax for travel in lower Manhattan is a clear illustration of the policy being applied, and the political challenges of putting it into place. I have to admit that I may have been going too far with the chocolate example, and I apologize if that is the case. But at the same time, I hope my graphic illustration of a direct consumer to consumer externality forever fixes this idea in your mind.

Dear Miles,

Thank you for sharing these lectures. I continue to appreciate them. Just a heads up on a typo at the beginning of this post: “no one can be made better off without making someone better {SHOULD BE “WORSE”} off”

Best, Juliette

On Tue, Mar 31, 2020 at 8:15 PM Economics for public policy wrote:

> MilesCorak posted: “In this seventh lecture of Economics for Everyone, we > address the nature of government intervention in perfectly competitive > markets. Perfectly competitive markets lead to efficient outcomes, in the > sense that no one can be made better off without maki” >

Oh goodness, that is a major typo. Thank you for catching it, I’ve made the correction.

Hi Everyone. I am sharing a set of three inter-related comments/questions 🙂

Comment 1: You mention early in the lecture that we discuss commodity markets as these can be reasonably expected to behave in a perfectly competitive manner. This makes sense to me. Commodity markets are not a type of market that most of us have direct experience, but I am aware that they function in particular ways. Which is why we discuss milk, coffee, oil, rice, wheat, etc.

Comment/Question 2:

In going over the comparative statics exercise from question 5 and, in particular, your discussion of ‘government purchases to support a particular price,’ I experienced a moment when my understanding of perfectly competitive markets coalesced. It is funny to me that my understanding of why perfectly competitive markets provide the most efficient outcome occurred in a discussion of government interference in a market. Near the beginning of the lecture, you mention the scenario, discussed further in, when private marginal costs/benefits don’t reflect social marginal costs/benefits. You note that this is often because, “something is missing in the market … usually imperfect property rights that leads to a failure, we may end producing too much or too little of goods.”

Arriving at the correct answer to question 5 involves appreciation of the notion that ‘the situation that maximizes the social surplus is the perfectly competitive outcome.’ So that in the example of the price support program where a target price is established/maintained by the government creating an artificial demand for a commodity, such as rice, by purchasing a certain portion of that being produced. Such a situation could arise if the producer of a commodity exerted political influence, wherein the government price support program is designed to benefit that industry. Under price supports, the cost to consumers goes up, so the primary (or, only) beneficiary would be the producer.

I am wondering if the case of agricultural staples might be a case where something might be ‘missing from the market.’ Or, if there might be special cases where the government might support an artificial target price to maintain a necessary sector of the economy. The use of rice as an example is what made me think of this. It would seem less convincing, to me, for commodities such as coffee or oil. When the government purchases ‘excess’ rice produced by U.S. farmers, this supports the farmers – if the farmers could not afford to grow the rice for the price it would fetch on the market. But, it is also to support the consumer – if the consumer requires a certain amount of rice to survive. The consumer might prefer rice at a lower price, but, they can afford the higher price. What they could not afford would be if there were no rice available at all.

The perfectly competitive market would, if the price was too low, drive farmers out of business. This would raise the cost the commodity, until, either: (1) the inability or reluctance of consumers to pay a particular price would then, in turn, drive the cost downward; or (2) the rise in the price the commodity fetched on the market would bring about the expansion of rice farms or new farmers into the business of growing rice. This increase in production would also drive down the price. Might it be that the intervention of the government, rather than being due solely due to political influence on the part of the farmers, could also result from the fact that the state would be unable to survive such constant fluctuations in this kind of commodity market, fluctuations which could result in farms constantly going out of business and/or large segments of the population going hungry.

Comment 3: Finally. you note that, since the government cannot simply re-sell the commodity on the domestic market, it often sends the rice abroad in the form of foreign aid. This is interesting, and it may illustrate a manner in which any social benefit experienced in the U.S. had simply been ‘off-shored.’ International Aid is seen by many to be an unalloyed good. In some cases, as famine or refugee camps, it may well be. There are examples, however, where it is not so simple. The U.S. during the 1990s, for example, was in the habit of ‘dumping’ excess U.S. rice production as ‘foreign assistance.’ Haiti, had been food sustainable but its domestic agricultural industry was unable to ‘compete’ with the, essentially free, rice arriving from the U.S. Thus, this food ‘aid’ which appeared, in the short term, to be a boon to the population is rather shown, in the medium to longer term, to be very damaging to the people of that country.

Sorry for being long-winded. I find it a challenge, expressing my thoughts concerning economics. I begin to see the utility of charts 🙂

Regards,

Robert

Robert, these are all excellent observations that I hope other students will read and reflect upon. Thank you very much. I’m glad they are part of the record.

I have often used the analogy in class that we are in some sense learning to ride a bicycle in taking an economics course for the first time. It is going to be a wobbly ride when we first get on, but with practice it gets smoother, and eventually we not only learn to ride smoothly, we can steer and go toward interesting directions, almost forgetting about the mechanics of keeping the bike moving. Great job, you are definitely moving along nicely.

I think the only thing I need to respond to is part of your second comment, where it begins with “I am wondering if the case of agricultural staples might be a case where something might be ‘missing from the market.’ Or, if there might be special cases where the government might support an artificial target price to maintain a necessary sector of the economy.”

This is a good point that requires more attention than I gave it in the discussion of this part of the assignment. After all, there are two things producers (and consumers) might be concerned about, and we were primed to think about them both from the earlier questions about coffee: not just the trend in prices, but the variability in prices. And you are in fact correct, it may be that what is required in these markets is price stability, or insurance. What is missing? Where’s the market failure? Well remember the two welfare theorems we talked about referred to an economy wide situation of perfect and complete markets, for every commodity, across space, across time, and across different possibilities in the future.

I mentioned this in class briefly, that we are also assuming complete insurance markets for all possible contingencies, and this requires that insurance markets work and we are able to attach a probability to each possible risk. If this is the case, market participants can take out insurance contracts with someone willing to provide insurance.

But this clearly not always the case. So, if I understand your comment correctly, yes, there may well be a missing market problem here, a market failure because of the absence of complete insurance markets. So producers need more certainty about market conditions, particularly since demand and supply are so inelastic making prices fluctuate significantly. There certainly is some capacity for them to to do this by self-insuring, diversifying their products for example. But you are right, one of the motivations for government intervention is to offer stable prices as a type of insurance.

The private insurance market will sometimes fail for two reasons. First, fundamental uncertainty in which a probability can’t be attached to every possible contingency in all future states. Think of the times we live in now? What was the probability of COVID19 a year ago? I’m not certain anyone could have put a probability to that risk and profitably sell contracts. Second, when events are highly correlated, impacting on a large fraction of the population all at once, insurance companies will go bankrupt. That is why insurers don’t cover events like natural disasters or wars. In these cases we call on our capacity to act collectively through government to get us through.

But of course, the point of the exercise is also to appreciate that a call for stable prices, often morphs into a call for higher prices, “fair” prices, by the producer. And often the rationalization from producers for support programs that lead to higher prices for them, to the cost of consumers, is that they ensure the availability of supply. Our job as economists is to use our model, and to examine the data, to appreciate when this is true, and when it is used to divert attention from rent seeking behavior that favors one side of the market to the detriment of the other.

What do you think? Does this make sense?

Hello. Yes, that does make sense. Your response encourages me. I am pleased to have made a pertinent observation. I sometimes feel irredeemably critical in my responses! Yet, I think this is just me trying to define the content of the subject and nature of the knowledge by feeling around the edges, testing the waters, exploring the terrain and I appreciate your substantive response to my enquiries.

Hi professor,

My question is related to the answer to the second part of our assignment that you offered in the lecture. As you mentioned, the answer to the question is simply, “let the invisible hand do its job”. I understand that this is a logic of economic efficiency, for which maximum social surplus can be achieved only in perfectly competitive conditions. But to be honest, I don’t find this answer satisfying. If leaving it up to the market to decide is the only true way, why bother with these models that describe the effects of different interventions? To eventually assume that they are not needed and they only disrupt perfect markets? Is social surplus the only measurement of potential benefits in economics?

I think climate change makes a good case here against that absolute approach of “let the market be” and I’m glad that you mentioned it in your lecture as an example. As we’ve all realized at this point, the threat that it poses needs to be addressed today and the market has known this for a long time already. If that’s the case, why do we need the Paris agreement and other external mechanisms as a proxy for adjustments? Should we believe in this absolute notion of the invisible hand and wait until it will provide the best solution, or is global warming a market failure that cannot be undone without outside intervention?

To be clear, I’m not asking these questions in a rhetorical way. I’m asking them because I want you to elaborate on issues of market failure and cases when the market shows inflexibility towards the new (and in this case, not so new) information. I believe that the lecture didn’t do justice to the topic.

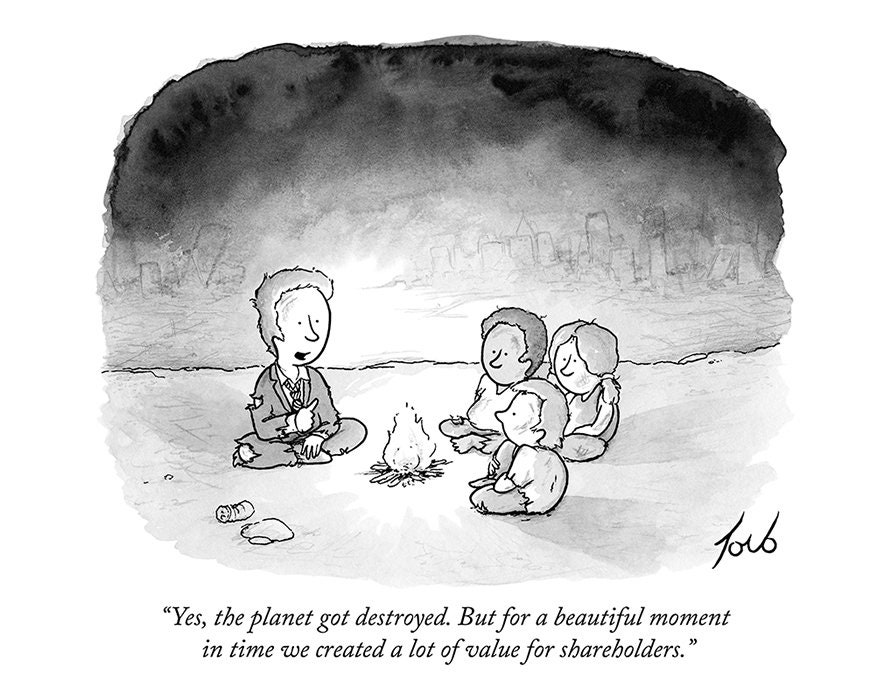

Lastly, I want to link this famous New Yorker cartoon which shares my sentiment.

Thanks for this George, this is a great question that gives us the opportunity to reflect on one of the themes in the lecture, possibly the major underlying theme.

We need to appreciate, using our model, when intervention can be socially beneficial, and when it reflects a capturing of government power that benefits only certain, possibly better organized, groups to the detriment of the social good. That is what I meant in drawing a distinction between “rent seeking” behavior, and interventions designed to address market failures.

So we study the agricultural support programs because they are an illustration of rent seeking behavior. Now, the assignment asks us to also look at expenditures and revenues under each program in order to figure out who gains and who loses. Clearly, in all cases market producers are able to get more money, and even more under some programs than under others. So they have an incentive to capture government policy to their benefit. We need our understanding of demand elasticities to be confident about this. Consumers of these commodities sometimes lose sometimes gain, depending upon which program. But in all cases the social surplus is lower, so that tax payers in general, many of whom might not be consumers or producers in these markets, will pay the cost. This is rent seeking behavior, and our tools help us to clarify what is going on.

But there is a separate rationale for government intervention, one that economists rely on. Government intervention is rationalized when there is a true market “failure”, and that is what the carbon pricing example is meant to illustrate since it corrects a negative externality. (Of course we are putting aside the whole issue of “government failure”, its capacity to design and implement a remedy, and the information required to get it right.)

We need to keep these two rationale for government intervention in markets separate in our minds, even though we can use the same tools to examine them.

Hope this helps.

George,

I agree with you. The aspect and examples I used in my comment was not externality but I’ve been feeling not comfortable with the notion that everything will work if we leave things on the free market.

Hi everyone,

Glad to be able to digest this information via youtube– particularly the discussion of quotas, price supports and deficiency payments. I wonder about the context of the historical introduction of these programs– if they don’t produce efficient outcomes, why were they used in the first place?

One might expect governments to hire the very best economists, who would in turn advocate for more competitive markets with more efficient outcomes leading to greater surplus for all involved. Are these programs just relics of 20th century economics schools looking to stabilize the effects of the free markets? As far as I can tell, quotas are still in operation in certain sectors of the economy– do these protectionist measures end up limiting GDP?

Rents are controlled in New York, which I would say is a good thing– a perfectly competitive housing market doesn’t sound like it would result in the best outcomes for everybody.

Hello Professor,

I have been grappling with the concepts of consumer and producer surplus.

I thought I would share my thoughts, leading to a question or two.

I created a couple of pictorial charts to help me visualize the concept, but I can’t figure out how to share them here… 😦

So, I’ll simply pose the question:

We can imagine the market demand curve being made up of a number of individual demand curves, a collection of ‘incremental marginal benefits.’

Visualizing this, it would appear that the first person to purchase a commodity pays the highest price. The second person pays a slightly lower price, and so on…

Of course, it makes sense that for very expensive commodities in which very few are produced – e.g. a Rolls-Royce or Ferrari – that these very few individual commodities would be very expensive.

But, when I mentally extrapolate beyond a luxury market to commodities with much larger and wider markets, I became a bit confused.

The consumer surplus exists in the space between the demand curve and the equilibrium point. If we define consumer surplus as the difference between what a person is willing to pay for a commodity and the amount they actually have to pay – the market price – then, it makes sense that this difference would be benefit or boon to the consumer who would be willing to pay $20 and only has to pay $15, because the market has settled at equilibrium. However, it leaves me with several questions:

a. What about the person who is only willing or able to pay the market price? Are they still considered to have reaped a benefit? This consumer would not have purchased the item at $16 or $17, and so cannot be said to necessarily have saved the difference.

b. What about the person who actually pays the higher, ‘original,’ price? That is, before the market establishes the market price at the equilibrium point. The eventual market price will be $15, but, before this occurs, the original price – in my imaginary example – is $20. This price, which helps us to determine what the consumer surplus is, must be paid by someone – an imaginary ‘original’ consumer… Presumably this person, or any other person who pays above the market price, has not ‘realized’ the consumer surplus.

Or, it may be that I am thinking about it the wrong way. As you say, ‘this is a market demand curve … the horizontal summation’ of all of our individual demands. So, that it may be that the idea of consumer surplus might be more applicable to larger aggregations of consumers than to the exact price paid by individual consumers – the consumer surplus thus only being able to be understood as a social surplus.

This is starting to make more sense, even as I ask the question… Perhaps, I should not think of consumer surplus so much even as the total benefits accrued by an aggregate of consumers in a perfectly competitive market, perhaps, as the benefits accrued by consumers as a group, being that groups share of the social benefit generated by a perfectly competitive market – the other share going to the producers as a group.

Thinking of the consumer surplus in these, social, terms makes the role of, and the effect upon, the individual consumer less central to understanding the concept.

I am sorry for late post. Thank you for your lecture. It helped me to be clearer especially about the notion of externality.

In the lecture video, I liked the moment when the professor takes out a chocolate, it reminded me of the moment that we had coffee beans coated with chocolate together in the classroom. Also, for me, it is better that I can see your face sometime in the lecture like this time.

My question is, when comparing the two programs, Price-support program and Deficiency payments around 35 minutes in the video, I just wondered why the government pays more with the latter program. In the case that demand is more elastic, doesn’t the government pay more with the price-support program than the deficiency payments?

In the part dealing with one of the answers to the question 5 of the assignment, it was said that the best way to benefit everyone is to leave it in the perfectly competitive market. I know it leads to a most efficient situation, but as discussed in the latter part like externality, if we let things rely on the market, there should be certain loss or someone who has to owe the loss or infliction and unfair situation. To use an example related to these days’ situation, since the demand for the essential products like hand sanitizers has risen, consumers would buy them even if the price of them become higher. In this case, in the perfectly competitive market, suppliers can decide to make the price higher and gain more profit. This leads to the situation in which many consumers, especially less fortunate consumers, benefit less. Indeed, that kind of cases had been found and this unfairly increasing the price was prohibited by the governments. Without this intervention, many consumers would have suffered more.