“The plan for today,” says Martin Feldstein as he begins his 8th lecture to the Harvard students enrolled in a course called American Economic Policy, “is to finish up my three lectures on monetary policy.”

It couldn’t come at a better time, because today [February 10th] Janet Yellen is offering testimony on monetary policy. The news stories seems to say she is “on the one hand and the other hand” in her thinking about the future. The labour market is improving, but she is worried about the future slow down because of economic developments in China. But our trade with China is less than 1% of GDP, so why change US policy?

The Fed has a problem, it is pursuing multiple goals, targeting low inflation but also maintaining full employment, but how do you deal with two goals when you have only one instrument? The Dutch economist Jan Tinbergen taught us that we need two instruments for two targets.

Well, I keep saying there is also fiscal policy, and the Fed should keep reminding Congress that they need help.

But operationally how does the Fed balance these competing goals?

The Taylor Rule

John Taylor of Stanford University suggested that interest rate should be set according to the inflation goal and the GDP gap. Taylor’s simple rule was close to what Alan Greenspan was actually using as the Federal Reserve chair without knowing it during the successful 1990s. (Economists called this period the “great moderation.”)

John Taylor of Stanford University suggested that interest rate should be set according to the inflation goal and the GDP gap. Taylor’s simple rule was close to what Alan Greenspan was actually using as the Federal Reserve chair without knowing it during the successful 1990s. (Economists called this period the “great moderation.”)

How to do it? In retrospect Taylor proposed a rule that is pretty close to what was being done. Not a hard and fast rule, but a guideline.

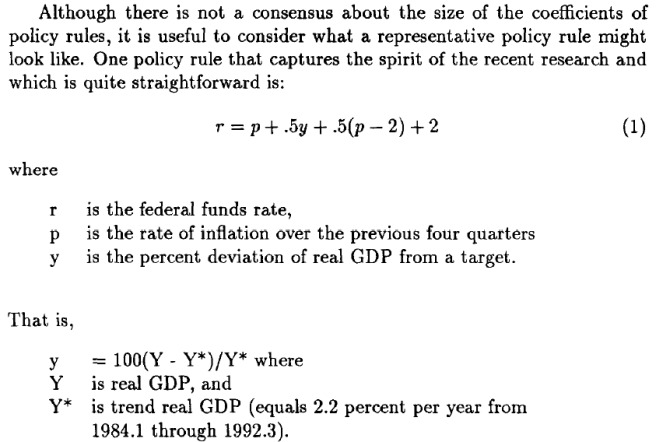

What exactly is the Taylor rule? The target for the Fed funds rate at a particular point in time should be equal to the sum of four things. First, the inflation rate. Then add to that 1/2 of the difference between the actual inflation rate and the target inflation rate. And then add 1/2 of the difference between actual and trend GDP (expressed as a percentage of trend GDP). And finally add 2%.

Taylor proposed a proportional GDP gap rather than the unemployment rate because the NAIRU can change over time, and rather than trying to guess its value it is easier just to smooth GDP relative to its trend.

If the inflation rate is at its target value, and the GDP gap is zero, there is no reason to adjust interest rates and the Federal Funds interest rate should be equal to the prevailing inflation rate plus 2%. In other words the real interest rate should be 2%. If the inflation rate is higher than target, then the interest rate should be raised.

There was no real rationale for 1/2, it is a nice round number. But subsequently Taylor and others looked at what Greenspan actually did between 1987 and 1999, and when the equation is estimated you get 0.53 and 0.76 as the two coefficients. so 1/2 was not too far off actual experience.

A crucial property is that if inflation goes up, then real rates go up. If inflation goes up by 1% then the target interest rate goes up by 1.5%, and the real rate is higher by 0.5%. If we ask what happens to the Federal Funds target rate when we change the inflation rate by 1% … well, it goes up by 1 + 0.5 and the real rate is higher by 0.5.

Before the early 1980s the Fed didn’t really understand the distinction between real and nominal interest rates. Real rates actually fell because interest rates did not go up enough during periods of higher inflation rates.

Between 1960 and 1979 inflation got out of control, rising from 2% to 10%. It was not that the Fed didn’t care, they just got it technically wrong. A Taylor equation for these periods finds that the inflation coefficient was 0.81. Interest rates did not rise enough. A big costly mistake because it allowed the economy to go from 2 to 10% inflation, and all the adverse consequences I talked about before. They thought they were tightening but they weren’t.

The Taylor rule tells us the Fed is going to keep real rates up as long as inflation is above target. This should create public confidence that the Fed will keep the inflation rate low. Also if there is below target inflation or if there is a GDP gap, then we would want to have a lower interest rate and a negative real rate. This would stimulate the economy in the way we talked about before.

Where is the Fed going?

This is a fall back rule to judge where the Fed has been. What would that rule apply now? How does what it implies compare to what the Fed says it is going to do going forward?

The inflation rate is 1.5%, the target rate is 2%, and I would say the GDP gap is now zero.

What does that imply for the target interest rate? According to the Taylor Rule it should be 3.25% (= 1.5 + 0.5(1.5-2) + 0 + 2). This is a starting point for a discussion about where the Fed should be going. But the actual rate is about 0.375%. Wow look at difference. I mean way the hell off. The Federal Fund rate may be too low, and many people feel it is too low. But the Fed says this was part of unconventional policy that we will correct over time.

If you go to their December statement they want inflation at 2%, and want to be at full employment and a fed rate of 4%. So in 2018/19 they want to be where the Taylor will take then, but they are adjusting slowly.

The Federal Reserve hates the Taylor Rule, and doesn’t want the rule imposed on them. There is a debate about this. Some members of the Congress want a standard that the Fed ought to achieve or explain why it doesn’t. They would like something like a Taylor rule, and if not an explanation of why not. This would not be a big deal, but it would limit the Fed’s discretion.

The rule communicates a commitment to price stability, and a return to trend. But it is a simple formula. If you read Yellen’s testimony you see she is thinking about a lot of things: future demand, non participants in the labour force. But the rule is backward looking. When she testifies she talks about what is happening in the rest of the world, and what is happening in the banking world. So life is more complicated in her eyes.

There are advantages of a rule even if it is a starting point.

The first advantage of having a rule is that it gives the public a sense of what the Fed is trying to do, and they need a sense that the guys and gals on Constitution Avenue have a commitment. The second advantage is that it disciplines the Fed. Whether by technical mistakes, or just focusing too much on unemployment and not inflation, the Fed in the 1960s focused too much on unemployment that led to much higher inflation. Something like a Taylor Rule would discipline the Fed. But it is not just the Fed that needs discipline. We know the federal budget is growing. If Congress sees only a low interest rate there is no discipline on them to contain fiscal policy.

Unconventional Monetary Policy

Okay, now I want to talk about unconventional monetary policy. How did Fed adopt it, was it effective, how is it going to move forward?

Okay, now I want to talk about unconventional monetary policy. How did Fed adopt it, was it effective, how is it going to move forward?

The US Federal Reserve came late to the game of the recession, driving the Fed rate down in late 2008, when it got together with Treasury. A good thing, but not enough, and fiscal policy was not stimulative enough. So Ben Bernanke used a new policy.

This involved large purchases of securities, of government treasuries, vast volumes of long-term securities. This was different. They also told markets that short-term rates would be low for a very long time. The point was interest rates were going to be kept low for a very long time. They knew this would drive long rates down. This reduced the yield curve.

The purpose was to stimulate home buying, and push up house prices. But more generally very low long rates would lead investors to move from fixed income (in bonds where they weren’t getting anything) toward equities, pushing up equity values and increasing household wealth and therefore consumption.

It actually worked very well but with vast unconventional policy. They were buying up bonds, and that exploded reserves at the Fed. The Fed would pay interest on reserves, so deposits increased tremendously because commercial banks got a safe return. Reserves held at the Federal Reserve went from $5 billion to $300 billion, and up to 2.5 trillion dollars.

This is sometimes called Quantitative Easing. They bought bonds from the public and banks. This did not increase money supply because the commercial banks deposited them at the Fed. So money supply did not go up, and inflation did not increase.

Why did it do this? Conventional policy was not working to increase the demand for housing and equities.

It did not work immediately. Bernanke warned about this. The pace of the recovery moved slowly even in first half of 2013. But in the later half of the year the stock market shot up as investors accepted low long rates, and similarly the price of homes rose. This increased wealth in 2013, which was 10 trillion dollars or about 3/4s of a year’s GDP. Think about the 4% rule of thumb that 1% higher household wealth increases aggregate demand by 4%. So in second half of 2013 the economy grew at an annual rate of 3.5%.

In the later half of 2014 growth was 4 to 4.5% and this got us to what I would say is full employment. We saw a brief drop of GDP growth in the fourth quarter, and the expectation for next year is growth of 2.5%.

There is a lot of talk about whether we going to have a recession, but boy I don’t see where this will come from.

Unconventional policy brings problems

Reaching for yield has led to a bidding up of the price of equities. The stock market is high. The price to earnings per share is historically at about 15 times. Today we are at 20 times. A third higher than historically. Share prices I would say are out of line where we would expect them to be.

With low interest rates it is not unreasonable to hold stocks. But the Fed has told us the alternative is changing. The Fed is expected to normalize interest rates, and we have to wonder if the price-earnings ratio will remain out of line.

Portfolio risk taking outside of equities is also a problem. Credit and duration risks are increasingly taken. Junk bonds can be taken, with a possible reward. The interest rate on junky-junk bonds was as high as 8%. Holding low quality securities, was also coupled with long-term securities which are also more sensitive to interest rate rises.

We see all of this and more recently we see an unwinding of the stock market, which is down 10% this year.

Same thing with emerging market bonds, interest rates have gone up on these.

A third source of risk created by unconventional policy relates to other lenders reaching for yield, for example by lending to less qualified borrowers through mortgages and car loans. Along with lending to riskier borrowers, also goes fewer restrictions on the borrower. Low convenient lending. The banks really want your business, and you don’t have to be on the hook to increase payments even if your ability to pay falls.

Creditors are taking big risks on long-term mortgages, for example at 3% for 30 years. This doesn’t make sense if treasuries are at 4%.

The fourth adverse effect of unconventional monetary policy is that it disguises the costs of the Federal deficit. Traditionally bond markets would discipline the government. Well this is gone because interest rates are so low on government bonds, essentially 0 at 10 years and beyond. Increasing the temptation for government to borrow more and allow the debt to rise.

Recently we are seeking a fifth problem because banks are in trouble. Bank stocks are collapsing. Banks make money by taking short-term deposits and lending it at higher rates at the long end. This spread relative to cost of funds is their profit. But there is no spread now. Profits are being squeezed by this unconventional policy.

The final risk is future inflation. The core consumer price index is increasing at 2.1%, that is okay. But we are at the point that inflation will increase because we have driven unemployment to the NAIRU. Recent wage increases are a warning.

Prices are being held down by low oil, and the energy component of the inflation index is down. But oil just has only to stop falling for the inflation rate to start rising.

With a quick rise in inflation the Fed may move more rapidly to get the Federal Fund rates higher. Right now the rate is negative even if they deliver on what they said in September.

Finally a few words on how the Fed raises the rate. If normal conditions prevail, this is easy through open market operations. But it can’t do that now. By buying treasury bills it will not have an impact because the banks already have tons of reserves. So the Fed can’t put pressure on them to borrow from the Fed or from each other because they have all the reserves they need.

Well the Fed could increase the interest rate on excess reserves. This creates a potential political problem. Remember it is holding on to $2.5 trillion in bonds. They are earning more on bonds than paying on reserves. If interest rate on reserves rises this could exceed earnings on bonds.

Now imagine Janet Yellen in front of Congress having to explain paying $50 billion to banks in order that they will raise the interest rates on households. That is a tough question to address, and I think the Fed will go through the back door by using Reverse Repos. They will duck the question this way so that it appears that the market is doing it not them.

It is a challenge for the Fed to reverse course. And my feeling is that they will move too slowly.

We are going to send you Janet Yellen’s testimony and I hope you will read it to get a flavour of some of this discussion.

One thought on “American Economic Policy, as told by Martin Feldstein at Harvard University: Lecture 8, Monetary Policy: Business Cycles and Inflation”