“The plan for today,” says Martin Feldstein as he begins his 8th lecture to the Harvard students enrolled in a course called American Economic Policy, “is to finish up my three lectures on monetary policy.”

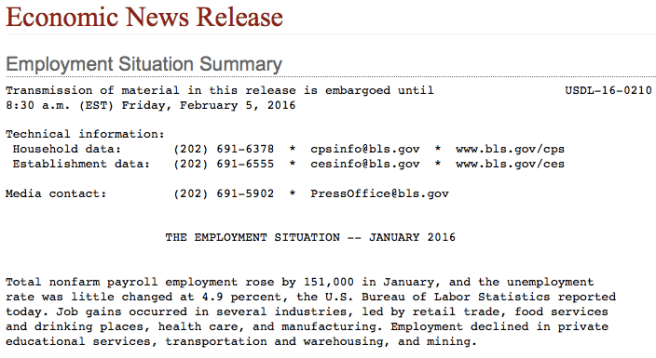

It couldn’t come at a better time, because today [February 10th] Janet Yellen is offering testimony on monetary policy. The news stories seems to say she is “on the one hand and the other hand” in her thinking about the future. The labour market is improving, but she is worried about the future slow down because of economic developments in China. But our trade with China is less than 1% of GDP, so why change US policy?

The Fed has a problem, it is pursuing multiple goals, targeting low inflation but also maintaining full employment, but how do you deal with two goals when you have only one instrument? The Dutch economist Jan Tinbergen taught us that we need two instruments for two targets.

Well, I keep saying there is also fiscal policy, and the Fed should keep reminding Congress that they need help.

But operationally how does the Fed balance these competing goals?