Top income shares have increased significantly in some rich countries, but not so much in others. In the United States the fraction of income going to the top 1% has more than doubled since the late 1970s. And while top shares have increased in other countries like Canada and the United Kingdom, they have not gone up all that much elsewhere, say in Germany or Sweden.

Globalization and technological change are often said to be the causes of growing inequality, but all rich countries have been confronted by these forces, and on their own they cannot account for the variation in top income shares between countries. A full explanation has to rely on institutions, policies, or norms of pay that differ across national boundaries.

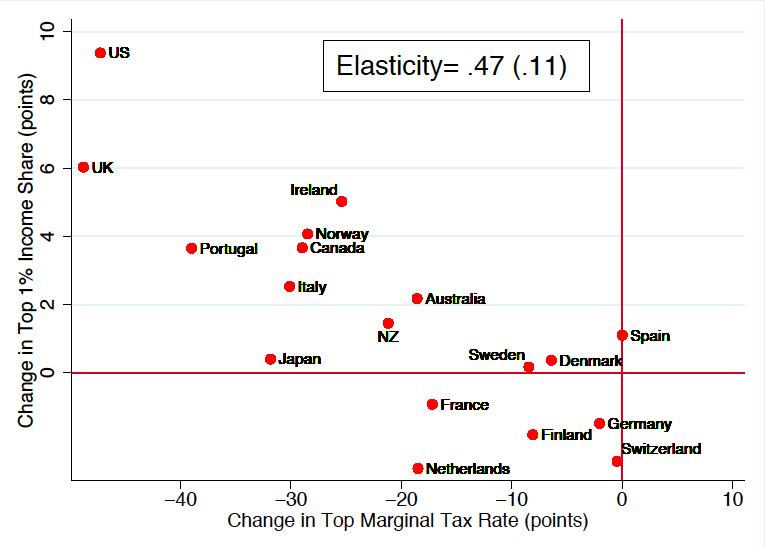

The first and most obvious place to look is at changes in tax rates.

Top income tax rates have certainly varied across the rich countries. But they have varied in a particular way: countries experiencing the largest falls in top tax rates have also experienced the largest increases in top income shares.

Facundo Alvaredo, Anthony Atkinson, Thomas Piketty, and Emmanuel Saez offer this intriguing picture in a recently released working paper called The top 1 percent in international and historical perspective.

Countries like the United States and the United Kingdom experienced very significant declines in the top income tax rates over a 40 year period—amounting to almost 50 percentage points—and also the largest increases in the share of income going to the top 1%.

In Germany, for example, there was hardly any change in tax rates, and also in top income shares.

One obvious interpretation is that cuts in tax rates spurred work effort, innovation and entrepreneurship among the most talented causing more economic growth, and greater individual earnings.

But the authors argue that this is likely an incomplete explanation. For one reason top income shares have not been correlated with higher growth. They examine a number of different perspectives, but note that top earners may simply have exercised more bargaining power to change how their pay is determined. With very high top marginal tax rates there isn’t much incentive for top executives to bargain for more compensation so they focus their concerns on other perks.

“When top marginal tax rates fell,” Alvaredo, Atkinson, Piketty, and Saez go on to hypothesize, “high earners started bargaining more aggressively to increase their compensation. In this scenario, cuts in top tax rates can increase top income shares … but the increases in top 1 percent incomes now come at the expense of the remaining 99 percent.” (page 5)

All this said, the negative correlation between top tax rates and top income shares could well be a coincidence, movements in both of them being caused by a third force.

The authors note that a shift in political power, reflected for example in the election of President Reagan and Prime Minister Thatcher, could well have led to legislative changes in taxes but also to deregulation—including the decline of unions—that may have implied an increase in top incomes.

A single picture can’t give us the answer to this question without an underlying theory of the causal forces driving the relationship, a theory that has to be articulated in a way that can be evaluated with more detailed data.

But the picture does pass the first litmus test that the authors put on any valid explanation—the need to account for differences across countries—and it thereby merits more detailed consideration.

One question I have about this is if these people have enough bargaining power to extract higher pay when tax rates go down, why wouldn’t they use it to extract pay increases to compensate for increasing tax rates?

They are taking a look at changes in top shares not just across countries, but over a long sweep of time. If I understand their argument correctly in the era of “managerial capitalism” of the post war period the concern was not just with remuneration but also firm growth. Further, they suggest that declines in tax rates interacted with globalization and actually increased bargaining power.

Hm. Then maybe it’s the globalisation that is the real driver, and tax rates just happen to be correlated with liberalised markets – especially liberalised markets for top executives.

You might have an interest in the paper, which is forthcoming in the Summer issue of the Journal of Economic Perspectives as a part of a collection devoted to the top 1%. The authors offer a more nuanced discussion, and treat a total of four different hypotheses. best m.

At a marginal tax rate of 80% it costs the employer $5 to increase the after tax income of the employee $1. At a marginal tax rate of 20% it costs the employer $1.25 to increase the after tax income of the employee $1.

Negotiations have two sides, so the employee should not be able to achieve the same after tax income under the high tax regime.

Further other perks will start to look relatively better under the high tax regime. Company cars, expense accounts, club memberships, short working hours, personal assistants, etc. The “Mad Men” lifestyle.

An interesting thing about these perks is that they are not portable. They are attached to the job and the company. If the job goes away, and an executive can’t get a similar package from another job, the perks go away.

Seems like it also makes it a lot more expensive to bribe government officials via consultancies and ridiculously highly paid jobs.

Miles, if it were true, as some argue, that tax cuts spur work effort and innovation – and hence drive up the incomes of the top 1% – we should also see an effect of tax cuts on growth (given the large share of top incomes in total GDP). But we don’t: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2029585 And neither do we see that highly unequal societies are high growth societies – on the contrary: http://filipspagnoli.wordpress.com/2013/05/27/income-inequality-28-bye-bye-incentive-theory/

However, one should perhaps look at total taxes, not just the top marginal rate. This rate determines just a part of the tax burden, and often a tiny one at that.

Interesting but I am slightly dubious about using the metric of the top marginal tax rate given that it is only a very rough proxy for the effective tax rate on the top 1%. For example, in Canada the reduced inclusion of capital gains and stock options in taxable income is a more important cause of the fall in the effective tax rate at the top. And sometimes eg the US the threshold for the top tax rate is higher than the top 1%.